![Bitcoin Cash [BCH] could be ready for another pump. Here's why...](https://www.blockchainnewsportal.com/wp-content/uploads/2023/08/Bitcoin-Cash-BCH-could-be-ready-for-another-pump-Heres-600x337.png)

The privacy landscape in crypto has changed dramatically over the past two years. Between regulatory crackdowns on mixers, the delisting of several privacy coins from major exchanges, and increasingly sophisticated blockchain analytics, the idea that crypto is inherently private is more outdated than ever. But privacy hasn’t disappeared entirely; it’s just shifted to different layers.

What’s Gone

Tornado Cash was sanctioned by OFAC in 2022, and the legal fallout is still playing out. Several privacy-focused coins have been delisted from regulated exchanges across the EU and parts of Asia. The tools that once offered strong transactional privacy for the average user are either unavailable, legally risky, or both.

Blockchain analytics firms have also gotten significantly better. Companies like Chainalysis and Elliptic can now trace transactions across multiple chains, identify patterns in swap behaviour, and flag wallets with high confidence. If you’re using a transparent chain like Bitcoin or Ethereum with any kind of identity-linked entry point, your transaction history is more traceable than most people realise.

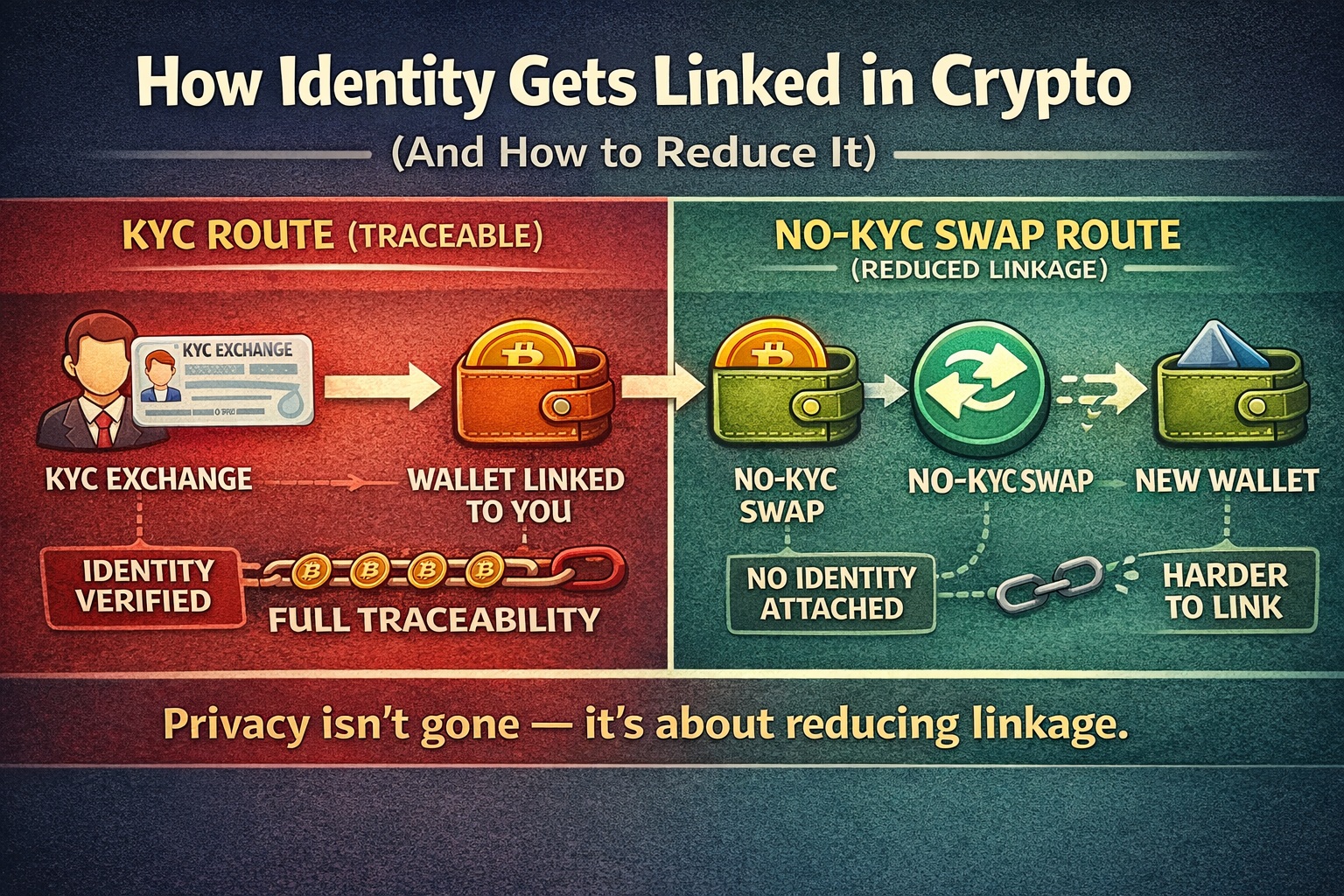

What You Can Still Control

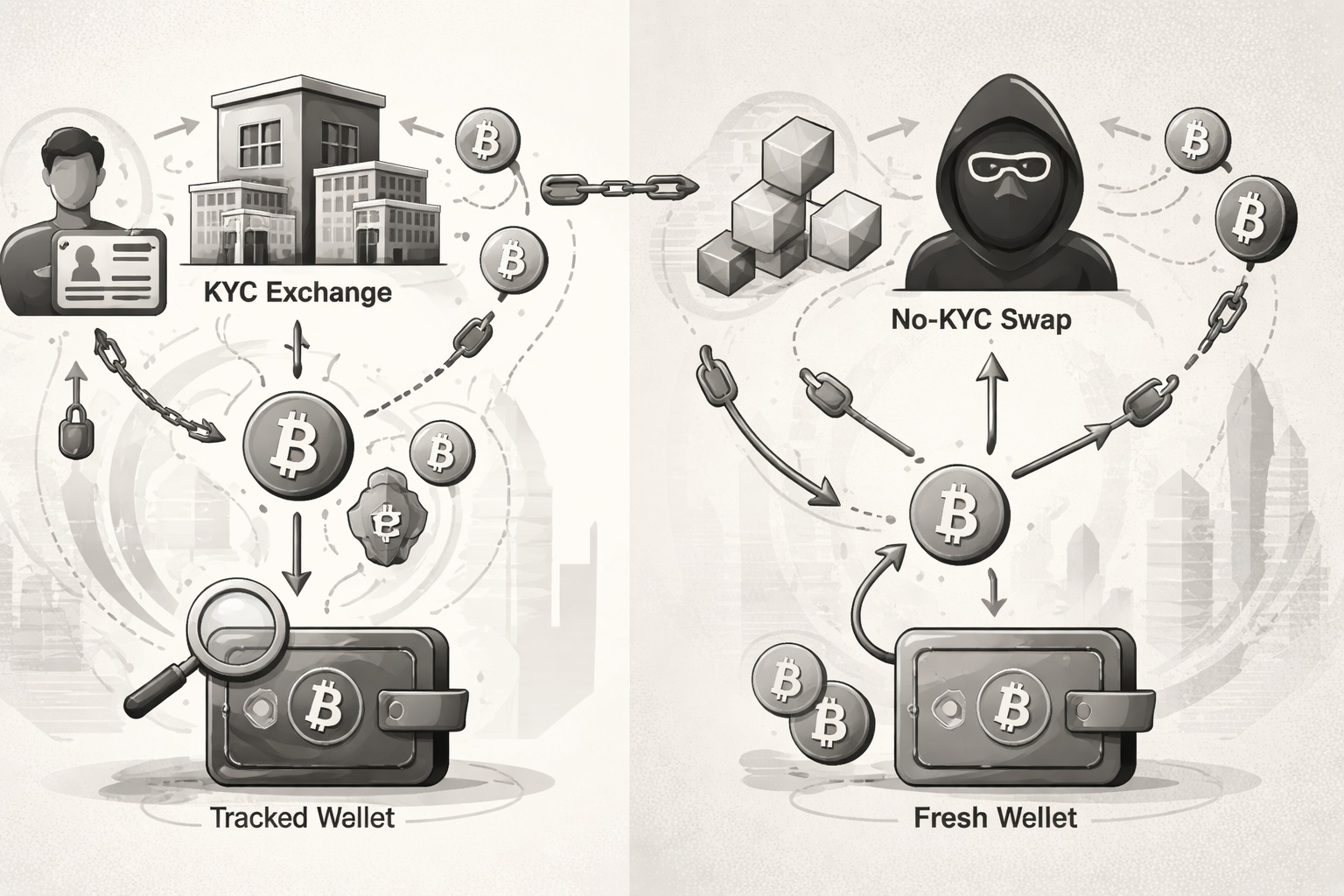

The most practical privacy measure is reducing identity linkage at the exchange level. Every time you use a KYC exchange, you create a permanent record linking your identity to a wallet address. From that point, every transaction that the wallet makes is associated with you. Using no-KYC swap services for crypto-to-crypto conversions breaks this chain. If your BTC enters a swap with no identity attached and exits as ETH to a fresh wallet, the link between your identity and the new funds is significantly harder to establish.

This isn’t about hiding anything illegal. It’s about basic financial hygiene. You wouldn’t give your bank statement to every shop you walked into, but using KYC exchanges for every small transaction is effectively the same thing.

Practical Steps for Reasonable Privacy

- Compartmentalise wallets. Using a single wallet for everything, receiving, spending, saving, and DeFi, creates a comprehensive financial profile on-chain. Separate wallets for separate purposes raise the effort required to link everything together.

- Use no-KYC swaps between wallets. When you move funds between your own wallets, a service like Paysmaker doesn’t require you to create an account or provide identification for most transactions. You swap without creating an identity record in between.

- Break patterns. If you always swap the same amount at the same time every week, that creates a pattern that’s easier to correlate across wallets. Varying your amounts and timing, even slightly, makes automated correlation harder. This is literally how analytics tools work.

- Mind your metadata. When you interact with a swap service via a browser, your IP address and browser fingerprint may be logged. Using a VPN doesn’t make your on-chain transactions private, but it prevents your web activity from being trivially linked to a specific wallet address.

- Choose networks deliberately. Some chains offer better default privacy than others. Transactions on networks with lower adoption or less analytics coverage are inherently harder to trace, though this is a moving target.

The Honest Reality

Perfect privacy on transparent blockchains is no longer achievable for most users without significant technical effort. But reasonable privacy, reducing unnecessary identity linkage, compartmentalising wallet activity, and using swap services that don’t require KYC, is still accessible and practical. The goal isn’t invisibility. It’s not handing over more information than necessary every time you move your own money.